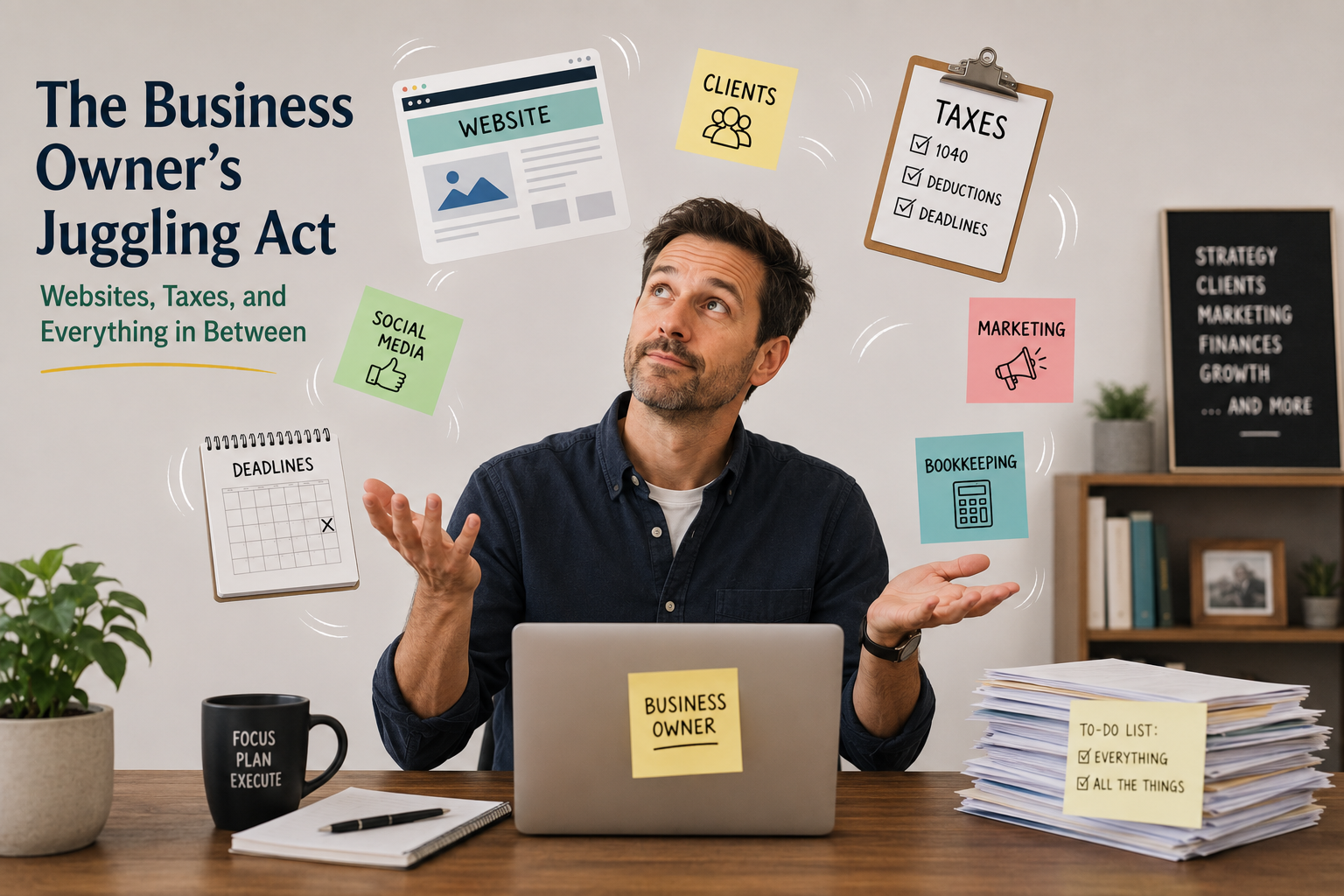

The Business Owner's Juggling Act: Websites, Taxes, and Everything In Between

Nobody warns you about the website.

You start a business because you're good at something — a trade, a service, a skill that people will pay for. You do the paperwork, set up an LLC, maybe print some business cards. And then someone asks: "What's your website?"

Suddenly you're watching YouTube tutorials on web design at 11pm, trying to figure out why your logo looks pixelated and whether you need a privacy policy. This wasn't in the business plan.

Welcome to small business ownership in 2026, where being good at your craft is just the starting point. The job now also requires you to be a marketer, a web developer, a customer service rep, a compliance officer, and somewhere in there — a bookkeeper.

Most owners handle the website eventually. It's the financial side that tends to quietly unravel while everything else is getting attention.

The Hidden Complexity of Running a Business

The challenges that blindside new business owners most aren't the big strategic ones. They're the operational details that pile up in the background:

How do I build a website that actually shows up on Google? Website builders like Squarespace and Wix have made it possible for anyone to get online, but SEO — the work that makes your site findable — is a discipline of its own. Keywords, metadata, page speed, backlinks: it takes real time to learn and maintain.

When do I need to pay taxes, and how much? If you're self-employed or running an LLC, you're responsible for quarterly estimated tax payments to the IRS. Miss them, and you'll owe penalties on top of the taxes themselves. Knowing what you owe — and having the cash on hand when it's due — requires clean, up-to-date financial records throughout the year, not just in April.

What can I actually deduct? The tax code gives small business owners legitimate deductions: home office, mileage, equipment, software, professional services. But claiming them requires documentation. A mileage log. Receipts. Properly categorized expenses in your books. Without that infrastructure, you're either leaving money on the table or guessing — neither of which is a good position to be in.

Am I actually profitable? This sounds like a question with an obvious answer, but many small business owners genuinely don't know. Revenue coming in feels like success, even when expenses are quietly eating the margin. You can't answer this question accurately without a reliable profit and loss statement — and you can't have that without organized books.

Why Bookkeeping Is the First Thing to Delegate

Every business owner has to make a decision at some point: what do I do myself, and what do I hand off?

Websites are learnable. Marketing is learnable. Even basic HR has tools that guide you through it. But bookkeeping has a compounding quality that makes DIY particularly risky. Mistakes made in January show up in April. Transactions that weren't categorized correctly in Q1 distort every report you run for the rest of the year. By the time you realize something is wrong, there's months of cleanup to do.

A bookkeeper doesn't just keep your records tidy. They give you something more valuable: clarity. When your books are current and accurate, you can see exactly where your money is going. You know what your margins are. You know whether you're on track for the quarter. You can make decisions from real numbers instead of gut feelings.

And when tax season comes, instead of dreading it, you hand your CPA a clean file. No shoebox of receipts. No months of reconstruction. Just organized records that make the filing process straightforward — and keep your accounting bill as low as possible.

The Practical Reality

Running a business in 2026 means accepting that you will wear multiple hats, especially early on. You'll figure out the website. You'll learn the basics of social media. You'll get better at sales conversations. That's all part of the entrepreneurial experience, and there's real value in building those skills.

But financial records are not the place to figure things out as you go. The cost of disorganized books isn't just time — it's money you didn't collect in deductions, tax penalties you didn't see coming, and decisions you made without the information you needed.

The business owners who grow sustainably are the ones who get their financial foundation right early. A dedicated business bank account. Clean transaction records every month. A bookkeeper who keeps it all in order so you can focus on everything else.

You don't have to do all of it yourself. The website, yes. The books — let someone else handle that.

If your financials need some attention, I'm here.

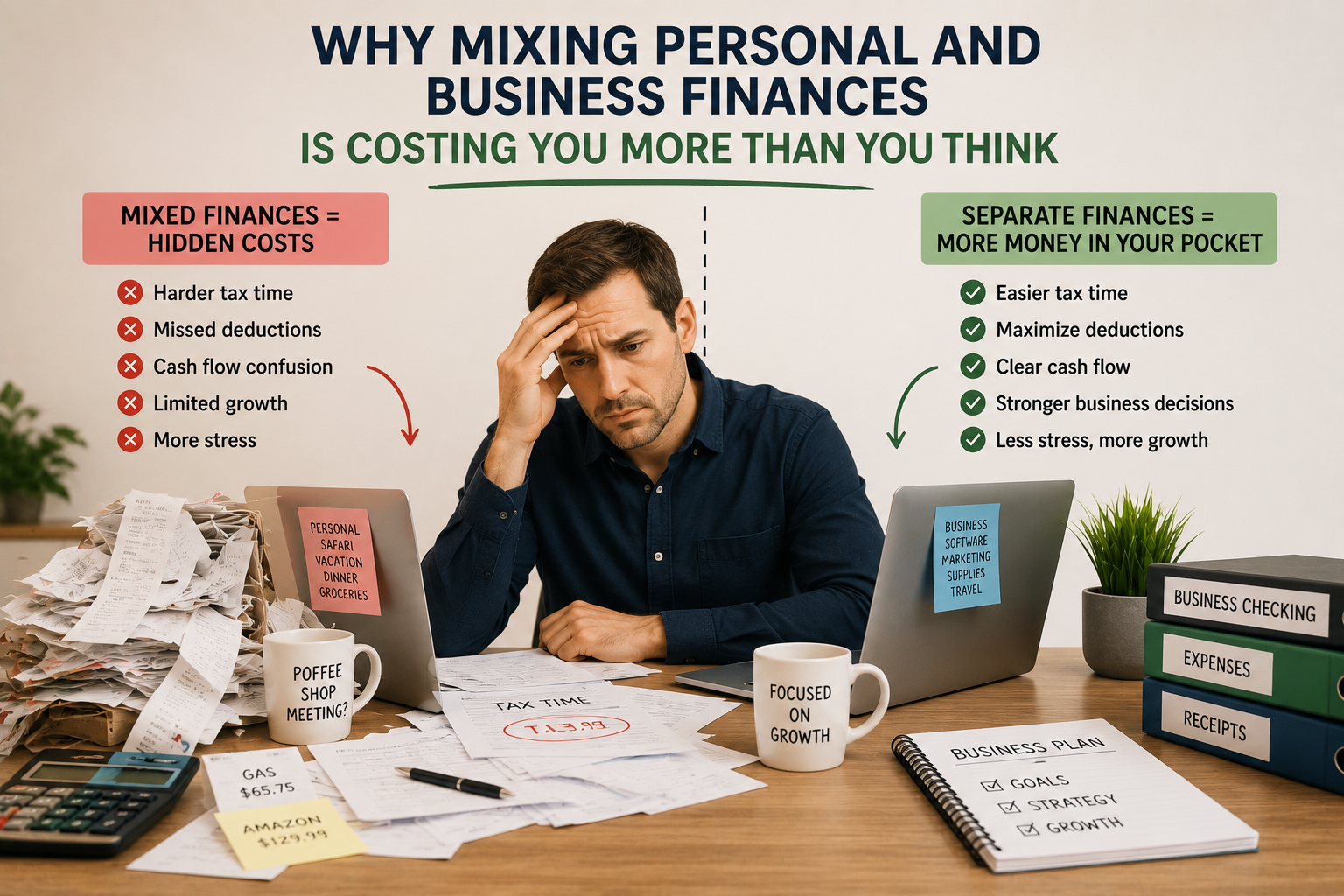

Why Mixing Personal and Business Finances Is Costing You More Than You Think

One of the most common mistakes I see small business owners make isn't a bad hire or a missed invoice. It's something far more mundane — and far more damaging.

They run everything through one bank account.

Personal expenses mixed in with business transactions. The occasional personal credit card used for a business purchase. A business account that doubles as a personal emergency fund when things get tight.

It seems harmless. Until it isn't.

The Hidden Cost of Commingled Funds

Most business owners who commingle finances aren't doing it out of carelessness — they're doing it out of convenience. When you're first starting out, opening a separate account feels like overkill. You know what's personal and what's business, right?

The problem is that your bookkeeper, your CPA, the IRS, and a judge in a liability case don't have that same context. They only see the transactions.

Here's what commingling actually costs you:

Your books become unreliable.

When personal and business transactions are tangled together, your profit and loss statement doesn't reflect reality. You might think you had a strong month — but how much of that revenue was offset by personal spending that never got categorized correctly? You can't make good decisions from numbers you can't trust.

Tax season turns into an expensive project.

Your CPA charges by the hour. When they have to reconstruct months of mixed transactions — figuring out which Amazon charges were office supplies and which were birthday presents — that's billable time that could have been avoided entirely. Clean books going into tax season can save you hundreds, sometimes thousands, in accounting fees alone.

You quietly erase your liability protection.

This one catches people off guard. If you're operating as an LLC, the entire point of that structure is to create a legal separation between you and your business. Creditors can come after the business — not your personal assets. But that protection isn't automatic. Courts look at whether you've actually been treating the business as a separate entity. Commingling funds is one of the clearest signals that you haven't been. It's called "piercing the corporate veil," and it can expose your personal assets — your savings, your house — to business liabilities.

The Fix Is Simpler Than You Think

You don't need a complex accounting system to solve this. You need three things:

A dedicated business checking account — used exclusively for business income and expenses.

A business credit card — for any business purchases that go on credit, earning rewards and keeping a clean paper trail.

A bookkeeper who reconciles the two accounts monthly and flags anything that looks out of place.

That's it. With those three pieces in place, your books are reliable, your CPA has what they need, and your legal protection stays intact.

Clean Books Start With Clean Accounts

If your financials are a little tangled right now, you're not alone — and it's fixable. The goal isn't perfection from day one. The goal is a clear, consistent system going forward.

If your books could use some clarity, I'd be glad to help.